Life Insurance Comparison

Choosing the right Life Insurance can be challenging. Conducting research using independent resources is a good place to start.

Canstar and Strategic Insight are two popular independent sources of comparison information.

We’ve provided information on their findings on how NobleOak compares to other insurers.

You can also click here to download our brochure on how NobleOak compares to other life insurance companies and why.

Canstar Awards

NobleOak award-winning cover is based on Canstar’s 5-star rating for best in class pricing and top-tier features. You can find out more by visiting our awards page.

Strategic Insight Research

Access research and information from Strategic Insights regarding Australian Life Insurance. You can view the reports here.

Comparing Life Insurance

Find out what to look for when comparing Life Insurance products. You can view more information here.

Strategic Insight research

Plan for Life (Actuaries and Researchers) is the leading independent supplier of Australian Life Insurance and managed funds market information, relied upon for over 20 years by the leading life offices, analysts, dealer groups and government bodies.

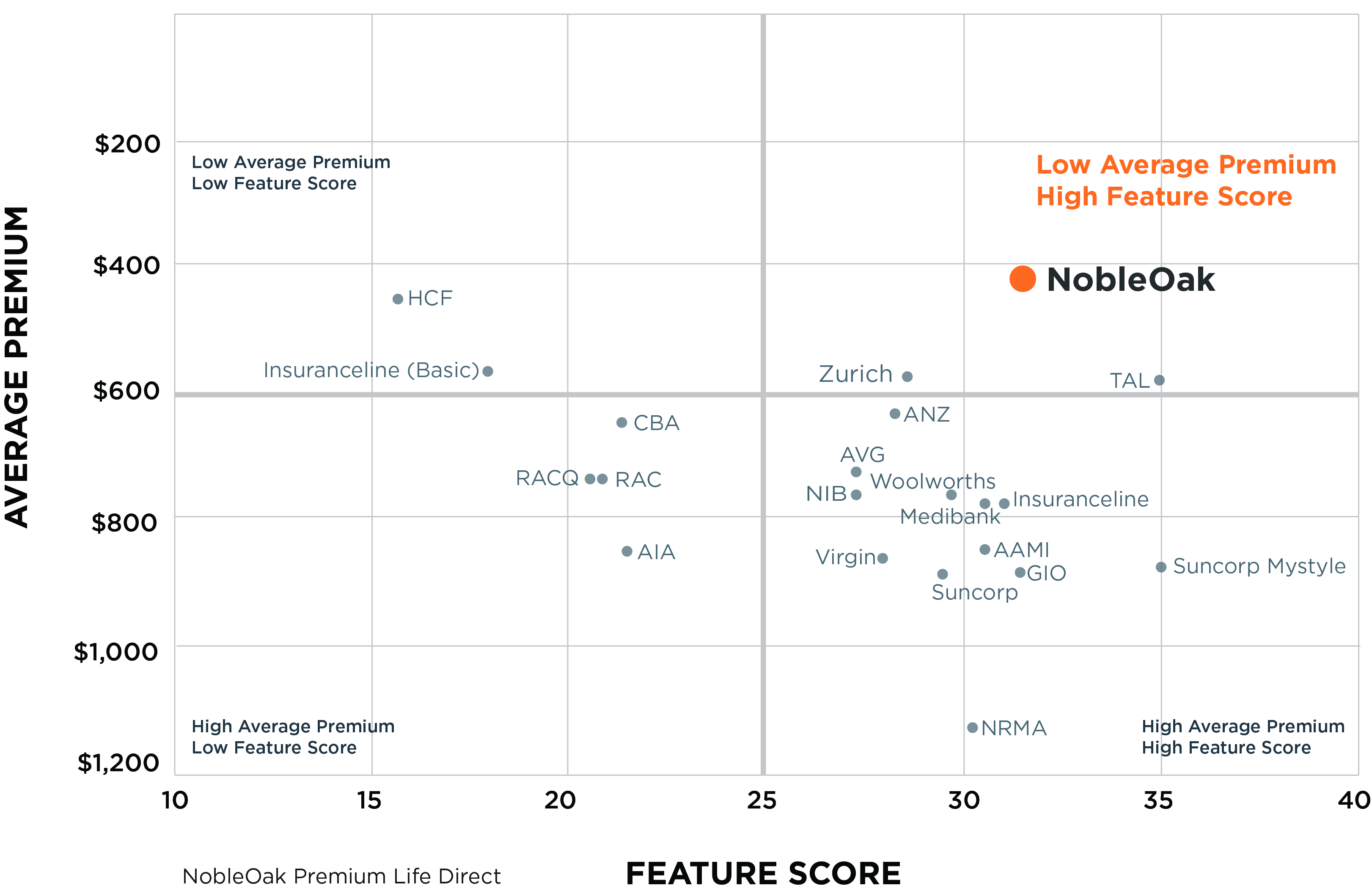

The Life Insurance cover provided through NobleOak’s Premium Life Direct product has been independently reviewed by Plan For Life. The matrix is prepared from information in the Plan For Life Direct Insurance Report 2020©. It clearly illustrates that NobleOak is a market leader with respect to price and features when compared to other Life Insurance providers.

Plan for Life (Actuaries and Researchers) is the leading independent supplier of Australian Life Insurance and managed funds market information, relied upon for over 20 years by the leading life offices, analysts, dealer groups and government bodies.

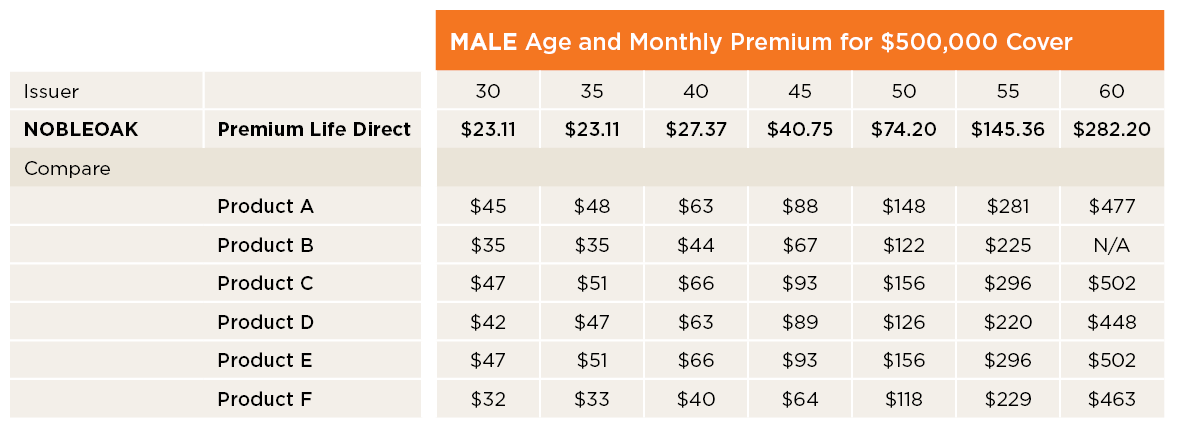

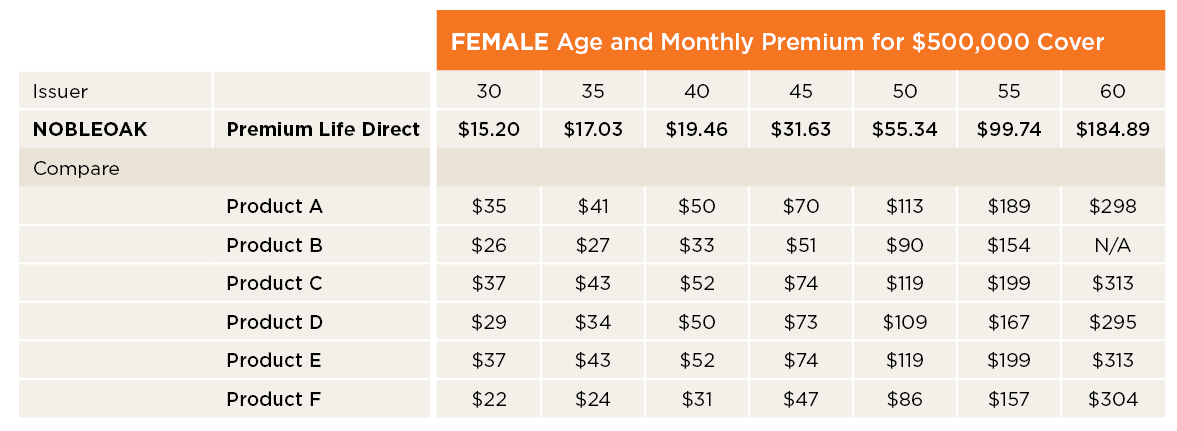

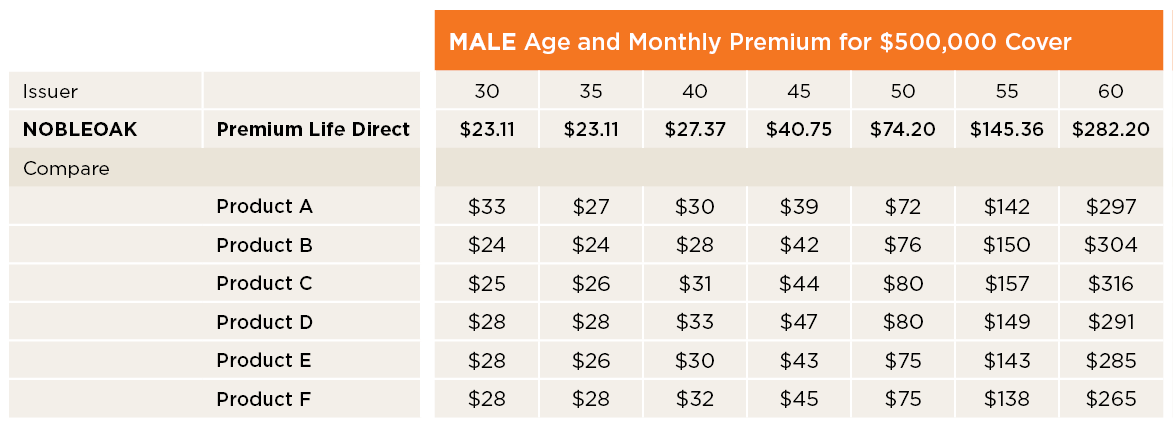

How our premiums compare

NobleOak offers similar comprehensive levels of cover as you would normally expect through a financial adviser or broker, at a competitive cost.

NobleOak offers similar comprehensive levels of cover as you would normally expect through a financial adviser or broker, at a competitive cost.

Our competitive Life insurance premiums are on average at least 20% lower than a range of major insurers based on a range of products purchased through an adviser and directly through the insurer.

The savings quoted are the average savings when comparing NobleOak’s premiums for its Term Life cover under NobleOak’s Premium Life Direct product to the average cost of Term Life insurance cover offered by a range of other Life Insurance companies, including products available directly from the insurer (6 products included in this comparison) and those available for purchase through a financial adviser or broker (6 products included in this comparison).

Notes for the comparison below:

- ‘Direct’ refers to Life insurance products available directly from an insurer, or a third party that does not provide financial advice.

- ‘Advised’ refers to Life insurance products available through a financial planner, adviser or broker, with the inclusion of financial advice.

- Direct products offer life insurance cover in a similar manner to Advised Products, however Advised Products may also offer other additional ancillary benefits and options.

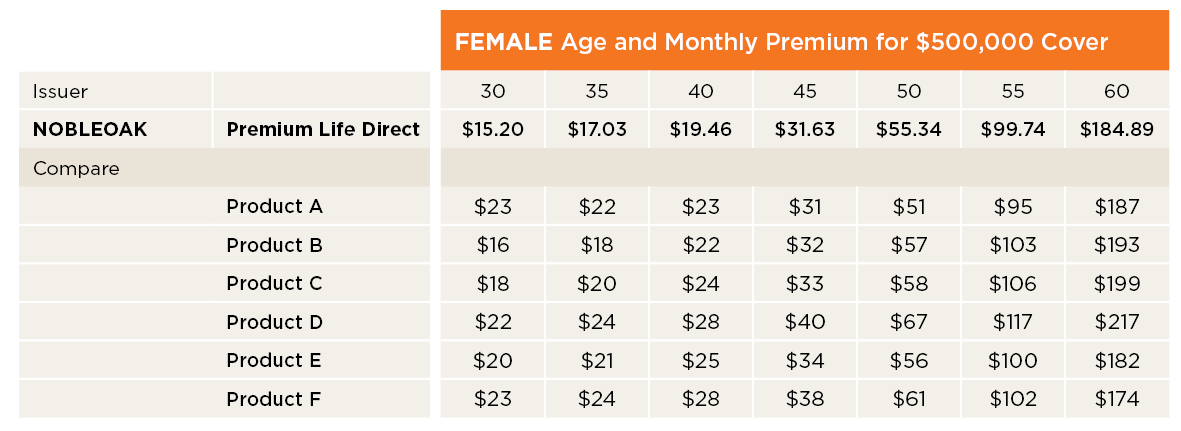

NobleOak vs Direct Life Insurers

The tables below illustrate how, based on premium rates available at 28th of April 2020, Plan for Life has calculated that for Term Life, Noble Oak’s Premium Life Direct product is on average 46% lower than a range of other comparable Direct Offerings (using an analysis of 6 products, Male and Female non-smoker White Collar workers with a Sum Insured of $500,000 and across 5 year age bands from age 30 to age 60).

Life Insurance rates for insurers, including NobleOak, may change in the future and this could change the outcome.

Plan for Life (Actuaries and Researchers) is the leading independent supplier of Australian Life Insurance and Managed Funds market information, relied upon for over 20 years by the leading life offices, analysts, dealer groups and government bodies.

NobleOak vs Advised Life Insurers

The tables below illustrate how, based on premium rates available at 28th of April 2020, Plan for Life has calculated that for Term Life, Noble Oak’s Premium Life Direct product is on average 10% lower than a range of Products available from Advised Offerings (using an analysis of 6 products, Male and Female non-smoker White Collar workers with a Sum Insured of $500,000 and across 5 year age bands from age 30 to age 60 for Advised products).

Life Insurance rates for insurers, including NobleOak, may change in the future and this could change the outcome.

Plan for Life (Actuaries and Researchers) is the leading independent supplier of Australian Life Insurance and Managed Funds market information, relied upon for over 20 years by the leading life offices, analysts, dealer groups and government bodies.

What to look for when comparing Life Insurance products

This is most often a key determinant as nobody wants to pay more than they have to. Bear in mind that even if the price looks right, if the product does not suit your needs or provide certainty of cover at claim time, then it may not be suitable for you.

If you are eligible for the cover

Although this won’t be an issue for most applicants, if you are above (or perhaps below) the eligible age limits or you have a particular health issue, then the cover may not be available in the first instance.

How much you can actually cover yourself for

Some Life insurers may only provide maximum cover up to $100,000 while others will provide an unlimited amount (subject to medical and financial requirements).

Factors which might prevent a claim being paid

Many savvy customers review all the ‘exclusion’ clauses within the Product Disclosure Statement (PDS) before they apply. For example, they check if there are any pre-existing medical condition exclusion clauses in the product. You may want to speak with your doctor about any exclusions before signing up for cover.

If there are any optional or built-in extras within the cover

Some products include valuable additional features. You could possibly be entitled to additional benefits such as automatic funeral cover, free financial advice or perhaps counselling for your loved ones in the event of your death.

How easily you can make changes to your cover

Your Life Insurance needs when you are 25 and single will be very different to when you are 45 and may have a partner, and possibly children, who are financially dependent on you. If there is little or no flexibility in the product to adapt your cover as your life changes, then it may not be right for you.

If you can include other Life Insurance covers

Cover such as TPD, Trauma, or Income Protection Insurance can often be bundled with your Life Cover. It’s important to consider all possible eventualities which could impact your own and your family’s financial future.